Certainly! Here’s a rewritten, cleaner, and more modern version of the content, preserving the original information and tone but improving readability and structure:

Delinquency Falls Amid Debt Renegotiations and Consumption Postponements; However, Pressured System Signals Risky Outlook for Brazil’s Economy

Brazilian households and companies together paid approximately R$ 1.148 trillion in interest throughout 2024, according to a study by the Federation of Commerce of Goods, Services and Tourism of the State of São Paulo (FecomercioSP). This figure marks a 17% increase compared to the interest paid in 2023, which totaled R$ 981 billion.

Most of this amount came from household budgets (R$ 859.9 billion), while companies accounted for R$ 287.9 billion.

These numbers indicate that the credit market continues to sustain aggregate demand, driven by credit growth and a significant drop in delinquency rates.

The reduction in delinquency, despite high interest rates, is a positive sign likely influenced by a strong labor market. However, there is an increase in household income and business cash flow being committed to debt payments. Moreover, Brazilian income is increasingly concentrated in the financial sector, which is concerning since real earnings are not growing at the same pace, creating a risky outlook for the sustainability of consumption and investments.

Higher Interest Rates, But Income Growth Remains Limited

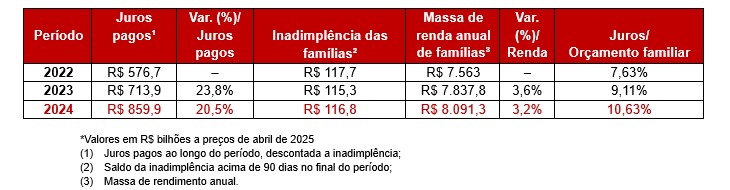

FecomercioSP’s calculations reveal that the amount of interest paid by Brazilian households in 2024 increased by 20.5% compared to the previous year, rising from R$ 713.9 billion to R$ 859.9 billion. In the same period, annual household income grew by only 3.2%, from R$ 7.838 trillion in 2023 to R$ 8.091 trillion in 2024 ([see Table 1]).

As a result, household budgets have become more burdened by interest payments: in 2024, over one-tenth (10.63%) of national household income was allocated to interest expenses, up from 9.11% in 2023. This is a negative indicator for the economy, as it diverts resources away from consumption and investments such as savings.

[Table 1]

Interest Payments — Households (2024)

Sources: Central Bank / IBGE / FecomercioSP

The delinquency rate has declined over the past three years, from 5.9% in 2022 to 5.26% in 2024. However, this drop reflects less about the average household budget’s health and more about systemic mechanisms such as credit turnover, debt renegotiations, and postponed consumption decisions.

[Table 2]

Credit Volume — Households (2024)

Sources: Central Bank / IBGE / FecomercioSP

Research data also show a 2.4% increase in the average monthly interest rate paid by households, reaching 3.58% in 2024 ([see Table 2]). This rise is modest compared to the 17% increase observed between 2022 and 2023.

Despite higher interest rates, the outstanding credit balance grew by 7.4% last year, reaching R$ 2.22 trillion. This suggests that strong consumption growth in recent years has been largely financed through credit.

Interest Rates Hamper Investments

Similarly, interest payments by Brazilian companies surged by 7.8% in 2024 compared to 2023, totaling R$ 287.9 billion. This growth came after a 21.9% increase in 2023 relative to 2022 ([see Table 3]). Meanwhile, delinquency balances fell 16.3%, from R$ 49.2 billion in 2023 to R$ 41.2 billion in 2024, with the delinquency rate dropping from 3.13% to 2.51%.

These figures reinforce recent analyses highlighting that financial costs remain a major obstacle to private investment recovery, alongside Brazil’s high tax burden. Interest expenses weigh particularly heavily on Small and Medium Enterprises (SMEs).

[Table 3]

Interest Payments — Companies (2024)

Sources: Central Bank / IBGE / FecomercioSP

The average monthly interest rate for companies remained stable at 1.61%, while credit with free resources grew 4.4% in 2024, reaching R$ 1.64 trillion.

Pressure on Fiscal Policy

FecomercioSP’s study underscores the importance of aligning fiscal and monetary policies to achieve inflation targets and enable the Central Bank (BC) to reduce the basic interest rate, the Selic.

Without fiscal adjustments, Brazil will likely face real interest rates of 7% to 8% for an extended period, which will suppress consumption and investments.

[Table 4]

Interest Payments — Households and Companies (2024)

Sources: Central Bank / IBGE / FecomercioSP

This dynamic is concerning given that the total interest paid by companies and households accounted for 9.8% of Brazil’s GDP in 2024 (R$ 11.7 trillion, according to IBGE). According to FecomercioSP, these figures illustrate a system under high pressure. The expected economic slowdown in the second half of the year could trigger a new cycle of rising delinquency.

If you need the content adapted for a specific format or further summarized, just let me know!